The Russian bear is a decidedly different animal: Russia's economy is signaling an oil price rally

Russia's economy been remarkably resilient to low oil prices this year, a fact that may well signal a coming oil price rally.

Even as the oil price outlook has become clearly bearish, Russia knows little fear. It’s defying the oil price hibernation with bullish economic outlook, the best-performing equities market, and even the best-performing currency against the US dollar.

And there’s something the average investor might not know: A strong performance by Russia’s equities market almost always precedes a crude oil price rally.

When you add to this the Russia and OPEC commitment to a new round of crude oil output cuts, the much-needed supply squeeze necessary to lift oil prices might not be far off.

So why does a Russian bear potentially signal a victory for oil bulls?

Because Russia is the single outlier among oil economies right now. By all logic, it should be reeling with the effects of low oil prices, but it’s not.

Russia’s is the quintessential oil economy, with oil and gas accounting for 60% of the country’s exports and more than 30% of GDP. Russia is the world’s third largest oil producer and the second largest producer of natural gas.

Even so, economic growth in Russia has been defying the global trend and appears to be in the pink of health.

Russia’s economy expanded 2.2% during the third quarter, with GDP growing 1.7% up from 0.9% in the previous quarter. An Al Jazeera report credits President Vladimir Putin’s Strategic Spending Program that was launched in 2018. That’s quite impressive considering that global manufacturing activity fell for the sixth consecutive month in October, marking the sharpest downturn in 17 years.

Also on rt.com Russia & OPEC agree on new oil production cuts to prop up global crude pricesBeing so dependent on oil sales, Russia has every incentive in the world to want to keep oil prices buoyant. Indeed, as Kirill Dmitriev, CEO of Russia’s sovereign wealth fund RDIF, recently told CNBC:

“We believe the oil price will be a significant influence going forward but due to our agreement with Saudi Arabia we believe that oil prices will be stable and the Russian market (is) poised for continuous growth.”

Dmitriev also hinted that Russia and OPEC were “ready to act” if necessary to ensure that oil prices remain stable.

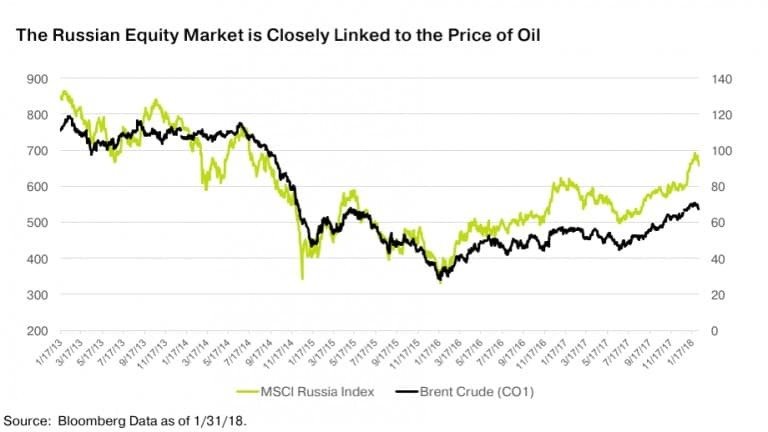

Given this backdrop, it’s not too surprising that Russia’s stock market has developed a very close relationship with the oil market. To wit, there has historically been a strong positive correlation between the MVIS Russia Index and oil prices, with one closely mirroring the other’s moves, sometimes with a lag of just a couple of weeks.

The good news is that Russia’s equity market is currently strongly bullish.

Russia’s RTS Index year-to-date (as of November 20th) is the best-performing stock market anywhere in the world. So far, it has boasted a +37% return in US dollar terms.

There’s also the matter of GDP, and Russia’s comparatively attractive debt dynamics and fundamentals. Russia’s debt-to-GDP ratio is just around 20%, which compares wildly to Brazil’s ~80%, for instance. And as of the end of November, the Russian Ruble was also the world’s best-performing currency against the US dollar.

So it’s definitely worth keeping an eye on Russia’s stock market because strong performance by Russian equities almost always precedes a crude oil price rally.

With Russia and OPEC committing to a new round of crude output cuts, the much-needed supply squeeze necessary to lift oil prices might not be far off.

Risks to the bullish thesis

There are significant risks to this bullish thesis, though.

First off, OPEC+ only committed to output cuts only through March 2020, and what happens after that is anyone’s guess.

Second, the last round was not that much of a success and we could be about to see more of the same.

OPEC+ has actually come about 180,000 b/d short of the annual target based on average production levels through November 2019. Mind you, the group still fell short despite Saudi Arabia’s aggressiveness mitigating the lack of alignment by other key producers and, of course, the massive supply disruption after the Saudi oil field attacks.

Also on rt.com Why 2020 could be a crisis year for refinersThe 24-member nation OPEC+, which supplies about half of world oil production, will need to remove about 300,000 b/d more to comply with the new target.

Then, of course, there’s the question of lackluster demand thanks to a synchronized slowdown by the global economy.

The new oil market has been defying well-established norms such as the Oil-Gold relationship.

Don’t be too surprised if the Russian Oil-Equities nexus becomes the next victim.

This article was originally published on Oilprice.com